Payroll taxes – taxes withheld from employees. It usually consists of 1601C or withholding tax compensation. Other companies also consider withholding tax expanded or 0619E as payroll taxes. Especially those companies that give commissions aside from basic pay.

Withholding Tax Compensation

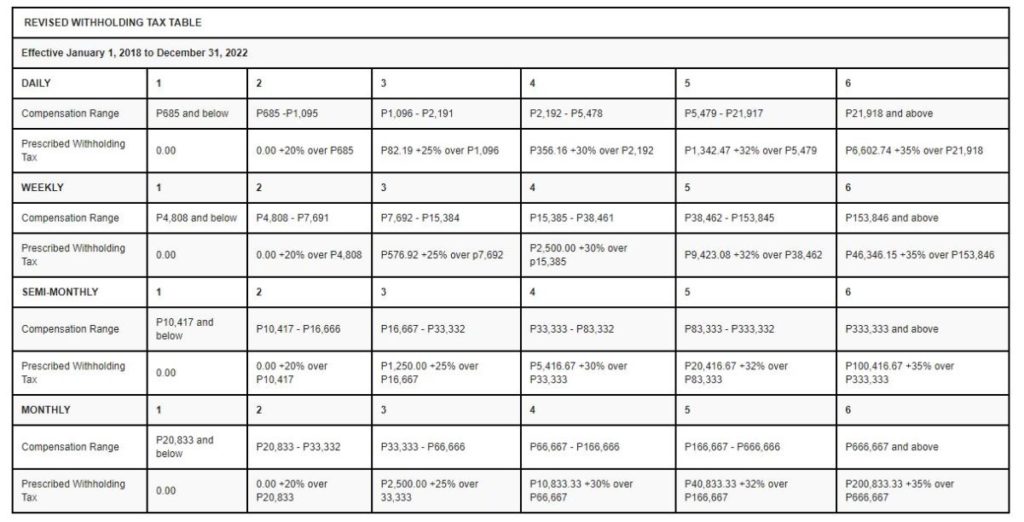

One of the payroll taxes is the withholding tax compensation or 1601C. Withholding tax compensation – the tax withheld from an employee’s income under an employee-employer relationship. It is usually the responsibility of the employer to withhold it from the employee and remit it to the government agency. Withholding tax table – used in measuring the withholding tax of an employee. The basis of tax is the basic salary. It also includes conditional supplementary like overtime pay, fees including director’s fee, profit sharing, monetized vacation leaves, and sick leave. Moreover, Taxable 13th-month pay, fringe benefit, and hazard pay.

Illustration:

For instance, minimum wage earner has no withholding tax on holiday pay. In addition, overtime pay, hazard pay, and night shift differential. Furthermore, tax exemption to 13th-month pay, SSS, GSIS, PHIC HDMF, and union dues (employee share). Moreover, other non-taxable salaries. Remittance of withholding tax compensation is monthly. 1601C or withholding tax compensation is due every 10th after the reference month for over-the-counter payment. While withholding tax compensation on electronic payment is due every 15th after the reference month. The final remittance of withholding taxes is on annual submission. The formula to compute the annual withholding tax is based on gross income. This includes the previous and present employer. Year-end adjustments will be on annual submission.

To get the taxable compensation income, non-taxable compensation will be less to the gross income. After deducting the non-taxable income, you now have the annual taxable income. To get the tax due, you have to deduct the withheld tax from January to November or the termination date. The total tax due will be a deduction from the last salary of the year. It will then be remitted to the bureau of internal revenue or BIR. If the tax due is break-even or equal, then there’s nothing to withheld from the last salary. But if the tax withheld from January to November / termination date is over then there will be a tax refund. The tax refund is usually given on or before January 25th of the following year. Withholding tax compensation rate range from 0 up to 35%. See table for guide.

See bureau of internal revenue (BIR) withholding tax table valid until 2022.

To see more on BIR withholding taxes click here

Withholding Tax Expanded

0619E or withholding tax expanded is a tax withheld from a certain income or commissions. Withholding tax expanded is creditable against the payee’s tax due. Some companies offer a basic salary for employees. And, on top of that is an additional commission based on sales performance or other conditions. The additional employee income is taxable and withheld by 10%. This tax is due every 15th day after the reference month.

Both electronic payment and over-the-counter payment are due on the 15th after the reference month. The employer should make an alpha list of withholding tax expanded every month/quarter/year. The employer should also give a copy of 2307 to every employee with commissions for a creditable tax. In a 2307 BIR form, the following information is needed, the tax period and tax payee’s identification number. Moreover, Payee’s name, registered address, zip code. In addition to that, the employer’s identification number, employer’s name, and registered address.

Other Additional Deductions Withhold from Payroll

Social Security System (SSS)

Another payroll tax is the social taxes or the Social Security System (SSS). Social Security System (SSS) – deducted from the employee’s income monthly. Social Security System (SSS) is a pension saving in the future. The monthly SSS contribution – also called monthly salary credits or MSC. The minimum MSC contribution is P2,000 up to P20,000 in 2020 raised to P3,000 up to P25,000 in 2021. The contribution rate is a total of 12% particularly 4% employee share and 8% employer share in 2020. SSS raised to 4.5% employee share and 8.5% employer share in 2021.

The contributions above P20,000 are deposited to SSS Provident Fund. The SSS Provident Fund is also called as Workers’ Investment and Savings Program. The deadline for payment of contributions is on the last day of the month following the applicable month. The employee who has a 2years contribution can have the privilege to borrow an sss salary loan.

Phil health

Is a deduction from the employee’s gross income. Phil health is health insurance. The employer usually withheld it from employees and will remit it to the government. Phil health rate is 3% of employee’s gross income in 2020. Philhealth’s contribution raised from 3% to 3.5% in 2021.

Pag –ibig

Pag-ibig is an employee contribution. It is a deduction from the employee’s gross income. Pag-ibig is a member’s individual savings fund. The pag-ibig member can withdraw its Pag-ibig savings fund after a certain period. The employee can also have the benefits to borrow from pag-ibig a salary loan and a housing loan. As long as the employee has a minimum 2years pag-ibig contributions. The employee can also withdraw the savings after 5,10,15 or 20 years. If not withdrawn, the employee can have the lump sum after retirement or at the age of 55 or 60.

Payroll deductions from employees are also withheld for the employee’s benefits in the future. Because these contributions are deposited to a specific fund for future use. The main purpose of contributions is for employees to have pensions in the future. Pag-ibig grants pensions to qualified employees monthly. To qualify, the employee should have a minimum number of years of contributions.

Otherwise, the employee should be at the age of 55 or 60. Some companies don’t provide retirement pay for employees. That’s why the government-mandated this contribution for the employees who happens to not have retirement pay. The deductions serve as contributions of employees are mandatory. Government mandates Pag-ibig contributions. The reason is for employees who don’t have a company retirement pay can have a pension. Pensions that can be used in the future when they are no longer able to work. But some companies are generous enough to set a retirement pay for faithful employees. If so, then the mandatory contributions will be a bonus for the employees. They may use it for whatever matter they want.

To learn more about payroll click here.

Need help? Get a free consultation.