Liabilities are an obligation. When we say liabilities, it is an obligation arising from either a contract, law, or a promise to pay. Now, what are the requirements for an obligation to be recorded as a liability to our financial statement? We have three requirements for an obligation to be included in the financial statement. Remember that not all obligations or credit are recorded in our financials.

Requirement Guidelines

1.) Present obligation

it means we have an unconditional promise or an obligation to pay. For accounting purposes, the first reason why we have an obligation is the legal obligation. When we say legal obligation, these are the liabilities arising from contracts, laws, or statutory requirements. Statutory requirements are obligations that came from the government. For instance, an Accounts Payable. We all know that accounts payable doesn’t have any written contract. But let’s not forget that a contract can be verbal or written. In addition, when we say contracts it is not necessarily a written agreement, as long as there’s a meeting of the mind. And in this case, accounts payable is a verbal agreement or verbal contract. Another example is the tax payable, SSS, Philhealth, and Pag-ibig Payable. These are legal obligations or statutory requirements by the government. Moreover, a liability arising from laws.

The second reason we have an obligation is the constructive obligation. The constructive obligation doesn’t come from a contract, laws, or statutory obligations. Moreover, the reason we have this constructive obligation is that we made a promise. And that promise to other individuals or entities creates a valid expectation. For instance, the company decided to give a bonus and they announce it to the staff meeting. They also added that it will be given together with the 13th month’s pay by the end of November. In this case, the announcement creates a promise and the employees have a valid expectation. As long as there’s promise and expectation. It is a liability.

2.) The obligation should come from the past transaction or past event

This guideline talks about past transactions or events. If there’s no obligating event or no reason why we incur an obligation, then there’s no liability. What does a past transaction mean? It is an event wherein we either gave or received an economic resource. For instance, a purchase of inventory. When the inventory is delivered then there’s the past economic event. Remember that a commitment does not create a liability. Because when we say commitment, it is merely an exchange of words, there’s no exchange of economic resources.

3. Settlement of economic resources

this is what we pay for the obligations. Normally economic resources that we pay are either cash or non-cash items like PPE or services.

Classification of Liabilities in the financial statement

1.) Current liabilities

These are the requirements of liability under the current section of the financial statement.

a.) The entity expects to settle the liability within the operating cycle. The operating cycle means from cash to cash. For instance, a trading liability. From cash, the company bought inventory. Then the inventory is sold. And we have accounts receivables. Then after that, the collection of accounts receivable. And finally, the accounts receivable will turn back into cash.

Generally, accounts payable is presented as current liabilities. Because it is a trading liability. And normally a trading liability is within the operating cycle.

b.) You should pay within 12 months after the reporting period. For instance, the reporting period is December 31, 2021. All payments made after the reporting period are classified as current liabilities.

c.) The entity holds the liability primarily for purpose of trading. This is for short-term liabilities. For example, the quoted financial instruments. Holding the quoted financial instruments short-term is like buying an inventory. The reason why you incur liability is to earn a short-term profit. When you sell it you can earn a profit.

d.) The entity does not have unconditional right to defer settlement. Remember when you have unconditional right it is current liabilities.

2.) Noncurrent liabilities

Based on standards when one of the current liability requirements is not met, the liability is presented noncurrent.

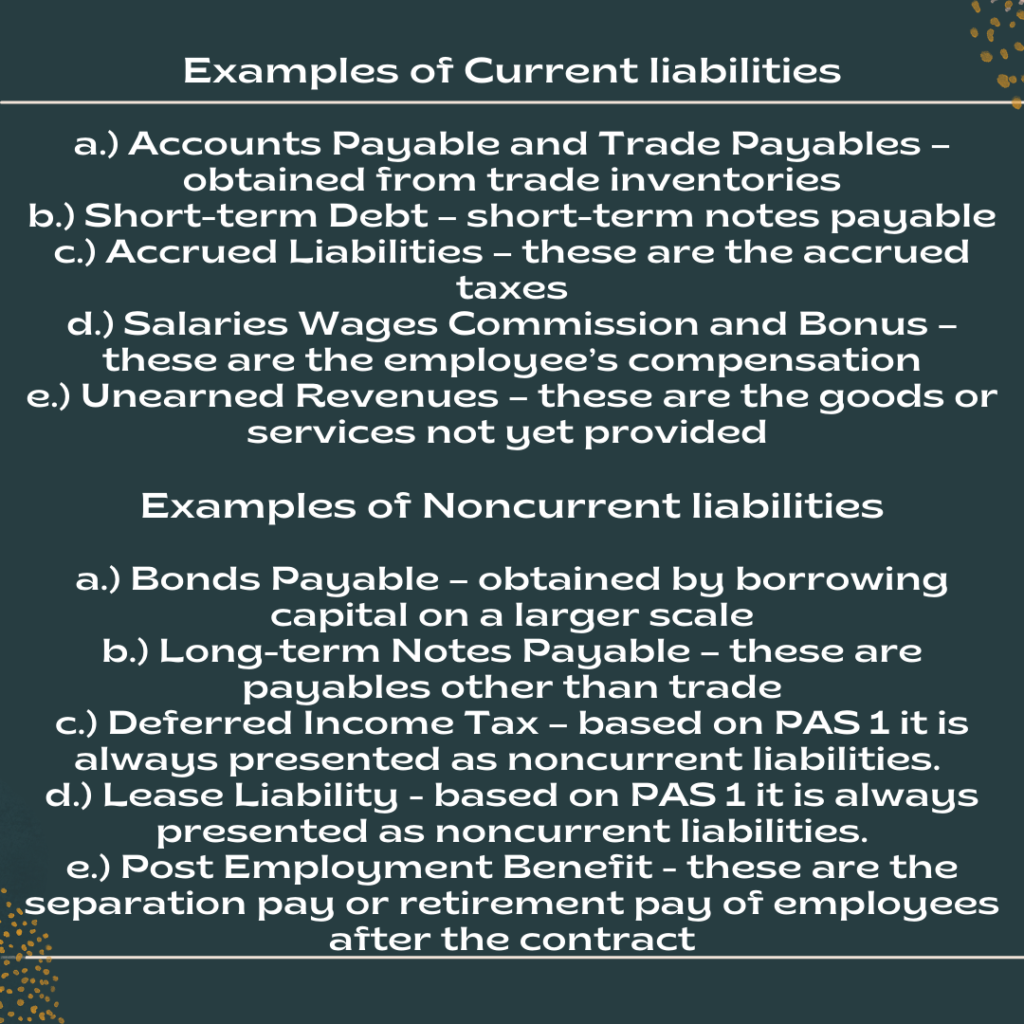

Examples of Current Liabilities

a.) Accounts Payable and Trade Payables – obtained from trade inventories

b.) Short-term Debt – short-term notes payable

c.) Accrued Liabilities – these are the accrued taxes

d.) Salaries Wages Commission and Bonus – these are the employee’s compensation

e.) Unearned Revenues – these are the goods or services not yet provided

Examples of Noncurrent Liabilities

a.) Bonds Payable – obtained by borrowing capital on a larger scale

b.) Long-term Notes Payable – these are payables other than trade

c.) Deferred Income Tax – according to IAS 1 or PAS 1 it is always presented as noncurrent liabilities.

d.) Lease Liability – liabilities arising from rentals

e.) Post Employment Benefit – these are the separation pay or retirement pay of employees after the contract

Conclusion:

Liabilities are an obligation with requirement guidelines. It may arise from legal or constructive obligation. A contract can be verbal or written. When one of the requirements is met, the liability is presented as current in financial statements. Otherwise, presented as noncurrent liabilities. And finally, the payment to settle liabilities is either cash or non-cash items.

Related Blog: Bookkeeping Services and Notes to Financial Statements

Do you need help? Contact us

Learn more about IAS 1 or PAS 1

Pingback: Warranty | Ronainph

Pingback: Bonds Payable | Ronainph