Depreciation is the cost allocation of a long-term asset. Long-term assets – used in more than one reporting period. It’s like your toothpaste, bar soap, and condiments. It’s good for more than one usage so you allocate the cost probably good for the whole month. Unlike the meals we eat, it is good for a moment therefore we charge the whole amount as an outright expense. No need to allocate the cost of one meal no matter how expensive it might be.

Three factors you need to know:

First, determine the correct acquisition cost of the long-term assets. The cost for depreciation must be correct. Otherwise, the depreciation expense is understated or overstated. It could somehow make the financial statements wrong especially if the amount is material.

Second, determine the estimated life of the asset. For instance, a truck is depreciated over its total mileage. In this case, the life of truck is the estimated total miles traveled. SYD is used as a denominator to get the fraction to be multiplied by monthly miles traveled. There will be no depreciation expense to any additional miles from the estimated total miles (denominator use). However, future purchase trucks will have new estimated total miles based on the previous experience of the same assets (truck). Remember that long-term assets like a truck are depreciated in different methods. In this example, we use the units-of-activity method. Aside from the units-of-activity method, we also have the straight-line method. In addition, the declining balance method, double declining, and sum-of-the-year method.

The third is estimated salvage value. Otherwise, residual value. It is the estimated value of the asset at the end of its useful life or upon disposal.

What is Depreciation?

Depreciation means the cost allocation of long-term assets. It is an expense account. The journal entry to record the expense is a debit to depreciation expense and a credit to accumulated depreciation. The normal balance of depreciation expense is debit. A debit to depreciation expense will increase and a credit will decrease the depreciation expense account. The normal balance of accumulated depreciation is credit. A credit to accumulated depreciation will increase and a debit will decrease the account. It is a contra asset account which means a deduction related to its asset account. Contra asset account – presented in financial statements next to the related asset account. Moreover, indented to emphasize that it is a deduction to its related account.

Depreciation conventions

1.) Nearest month convention – depreciation is based on the approximate acquisition month of the asset.

2.) Full-year convention – full depreciation on the year of acquisition. In addition, no depreciation on the year of disposal.

3.) Half-year convention – Half-year depreciation on the year of acquisition and the year of disposal

4.) Last year convention – No depreciation on the year of acquisition and full depreciation on the year of disposal

Methods of Depreciation

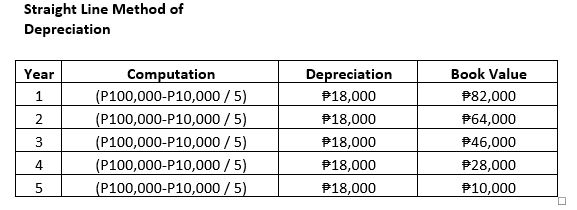

1.) Straight Line Method

The computation of the straight-line method is equivalent to cost less salvage value over its useful life. Depreciation ends when the asset reached the salvage value. Otherwise when fully depreciated. Most of the companies used the straight-line method. Because it is easy to compute. Moreover, its corresponding values.

Illustration:

Given:

Cost of an asset (Office Equipment) – P100,000

Useful Life: 5 years

Salvage Value: 10,00

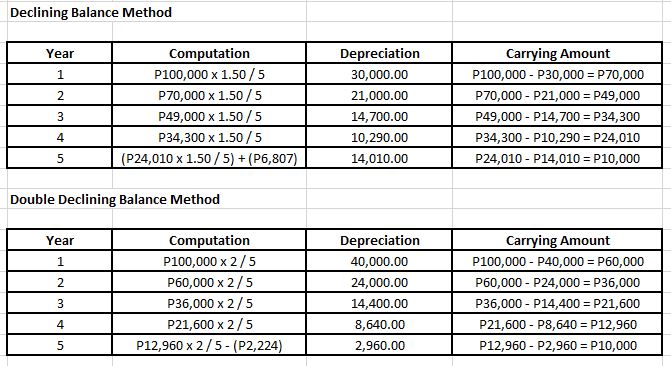

2.) Declining Balance Method

The formula of the Declining balance method is carrying amount multiplied by the rate over its useful life. Carrying amount means the book value of an asset. Often called the accelerating method. Because the depreciation is higher in the early years. And lower in later years. Some companies prefer this method because of the reason that assets perform best during the early years. Moreover, the output is greater during in early years.

Illustration:

Illustration:

Given:

Cost of an asset (Office Equipment) – P100,000

Useful Life: 5 years

Salvage Value: 10,000

Rate: 150%

Computation of Declining Balance Method and Double Declining Balance Method:

Note: Salvage value is not included in the declining balance method. Notice that the adjustment is made at the end of its useful life to end with the estimated salvage value. Instead of P5,880, the depreciation is P9,600. The double-declining balance method is almost the same as the declining balance. Instead of 1.50 multiply by 2.

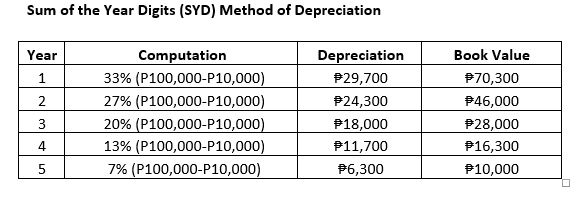

3.) Sum of the Year Digit (SYD) Method

SYD is computed first in this method. SYD is the total descending useful life of the asset. For instance, the SYD of 5 years is 15 computed as (5+4+3+2+1=15) or n(n+1)/2 where n is the total estimated life. Cost allocation expense is equal to cost less salvage value multiply by remaining useful life over SYD. Otherwise cost less salvage value multiply by SYD rate.

Illustration

Given:

Cost of an asset (Office Equipment) – P100,000

Useful Life: 5 years

Salvage Value: 10,000

Rate computation:

1st Year: 5/15 = 33%

2nd Year: 4/15 = 27%

3rd Year: 3/15 = 20%

4th Year: 2/15 = 13%

5th Year 5: 1/15 = 7%

For a total of 100% Table of computation

Related blog: Depletion and Bookkeeping Services

Learn more about cost allocation

Do you need help? Get a free consultation. Contact us now.