This content will teach you how to record wasting assets and their depletion expense. Similar to depreciation and amortization, depletion is an expense account. It is a deduction to gross income. Some companies selling the resources while extracting record it as an inventory. This way of recording is acceptable. If this is the case, inventory is an asset account. Recording it as an inventory involves a cost of sale account. The cost of sale is a deduction to gross sales. The effect is the same. It decreases the gross income/sales. Journal entry to record depletion is a debit to depletion expense and a credit to accumulated depletion. Alternatively, a debit to inventory and a credit to accumulated depletion. Then a debit to cost of sale and a credit to inventory at the time of sale. The cost of sale represents the depletion expense.

Wasting Asset

Wasting assets – also known as natural resources. When we say produce by nature it means it is irreplaceable. These are material objects with economic value and utility to man produced by nature. Once extracted and consumed, it will take more time to regenerate.

Depletion in Wasting Assets

Depletion is a counterpart of depreciation in property, plant, and equipment (PPE) and amortization in intangible assets. These three have a similarity. Depletion is the removal, extraction, or exhaustion of a natural resource. Moreover, it is the cost allocation of wasting asset depletable amount over the period it is extracted or produced. The depletable amount is computed by the cost of wasting asset less salvage value. The accounting method normally used for depletion is the output or production method. Depletion expense is equal to the rate multiply by units extracted during the year. Depletion expenses vary depending on the number of units extracted during the year. The higher the units of production the higher the depletion expense. In addition, the lower the units of production the lower the expense.

The depletion rate is equal to the cost of wasting asset less salvage value over its units estimated to be extracted. The rate is fixed unless there’s a change in the accounting estimate. The rate is not affected by the period it started even it started in December, the computation of depleted amount is still the same. Unlike depreciation, if it started in December, the depreciation expense is prorated within the year. The composition of wasting assets is the acquisition cost, exploration cost, development cost, and restoration cost. The first three are incurred at the beginning while the restoration cost is after the extraction. Restoration cost is computed at its present value. These four costs are capitalized meaning added to the cost of wasting assets.

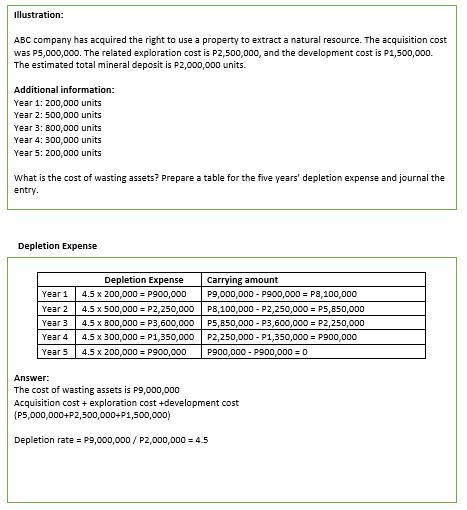

Illustration:

ABC company has acquired the right to use a property to extract a natural resource. The acquisition cost was P5,000,000. The related exploration cost is P2,500,000, and the development cost is P1,500,000. In addition, the estimated total mineral deposit is P2,000,000 units.

Additional information:

First year: 200,000 units

Second year: 500,000 units

Third year: 800,000 units

Fourth year: 300,000 units

Fifth year: 200,000 units

What is the cost of wasting assets? Prepare a table for the five years’ depletion expense and journal the entry.

Answer:

The cost of wasting assets is P9,000,000

Acquisition cost + exploration cost +development cost

(P5,000,000+P2,500,000+P1,500,000)

Depletion rate = P9,000,000 / P2,000,000 = 4.5

| Depletion Expense | Carrying amount | |

| Year 1 | 4.5 x 200,000 = P900,000 | P9,000,000 – P900,000 = P8,100,000 |

| Year 2 | 4.5 x 500,000 = P2,250,000 | P8,100,000 – P2,250,000 = P5,850,000 |

| Year 3 | 4.5 x 800,000 = P3,600,000 | P5,850,000 – P3,600,000 = P2,250,000 |

| Year 4 | 4.5 x 300,000 = P1,350,000 | P2,250,000 – P1,350,000 = P900,000 |

| Year 5 | 4.5 x 200,000 = P900,000 | P900,000 – P900,000 = 0 |

Note: Carrying amount is the cost or the remaining cost of wasting assets.

Conclusion:

You have learned that wasting assets are a natural resource. It is irreplaceable, and to recognize it is to deplete. In addition, the cost is compost of acquisition, exploration, development, and restoration cost. There’s two way to record the cost allocation of wasting assets. One is by the expense, and the other is by inventory. And lastly, the accounting method used to deplete wasting assets is the output or production method

Related Blog: Depreciation and Property Plant and Equipment

Learn more about Wasting Assets

Do you have a question? Need help? Contact us

Pingback: Depreciation | Ronainph