Bookkeeping vs Accounting is a topic that needs further discussion to emphasize the similarities and differences between the two. Bookkeeping is the identification of financial transactions relevant to the business firm and records by a bookkeeper.

Accounting is the bookkeeping process plus summarizing, preparation of financial statements which will be interpreted by an accountant to end-users. The one who records the transactions of a business is the bookkeeper. The accountant takes care of the rest.

Why there’s a need to compare bookkeeping vs accounting?

Comparison of two things is useful because it gives insights and comprehension. Hence bookkeeping vs accounting is one. Besides, it is one of the most searched phrases when it comes to business topics. People need to compare the two to understand the details better. Sometimes they create an argument about it. This is to determine the degree of truth to provide better meaning and conclusion. Bookkeeping vs Accounting is a broad topic.

Reasons of comparison:

1.) Similarities and Differences – bookkeeping vs accounting is similar when it comes to identifications of financial transactions and recording. Both used generally accepted accounting principles (GAAP), and both agree and follow the same process, cycle, methods, principles, and standards.

On the other hand, the bookkeeping vs accounting difference is that bookkeeping is limited to the identification and recording of transactions only. However, accounting can do both identifications and recording transactions plus prepare financial statements and interprets them for end-users. In addition, accounting is the higher form of bookkeeping, it is the advanced or complicated version of bookkeeping.

2.) Better Understanding – When two things are compared, the more it emphasizes the meaning or definitions. Moreover, we can identify the significance of one to the other. For instance, the lemon and lime are both acidic and sour, it is also both citrus family. On the contrary, it differs in scents and size. When these two are compared the significance is easy to remember and we can have a clearer understanding.

3.) Concise Meaning – Most people want to learn quickly or in a short time because time is gold and life is short. As a result, people who know bookkeeping and accounting try to compress the whole thing as briefly as possible. The purpose is to help other people have an idea. It is also one of the reasons why there are people who spend their time studying one thing. Furthermore, to be good at it to be able to summarize it for the world to benefit.

Bookkeeping vs Accounting

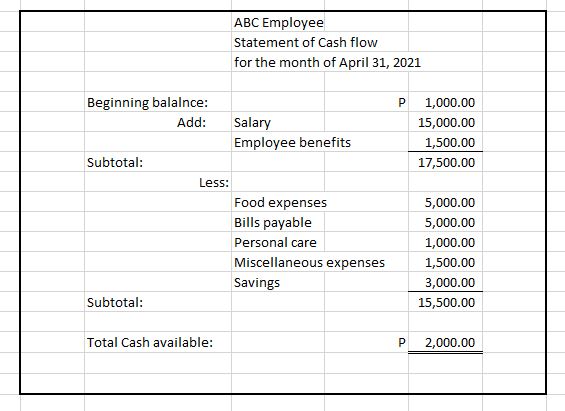

Bookkeeping is one of the accounting processes, it is a tool used to measure an individual’s net worth. For instance, an employee has a regular income and expenses. When an employee spends money he needs to identify where the money goes. By doing so, he is doing bookkeeping. Identifying where the money goes is called preparing a statement of cash flows. Statement of cash flows is the movement of cash. It should have a beginning and ending balance of cash available for use

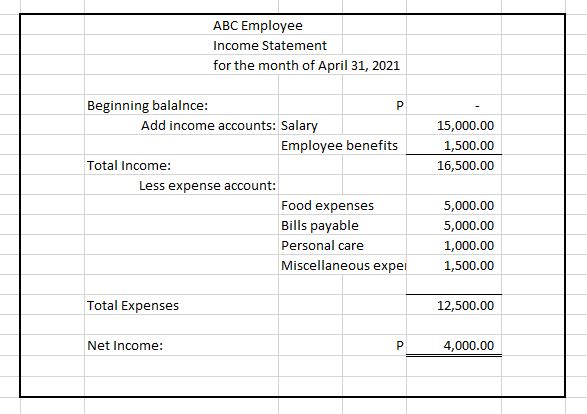

When an employee identifies where the money goes or the cash-out, it should have an equivalent. The cash-out equivalent could be an investment or an expense. Let’s say the cash out is an expense, usually, several expenses should match overall income. The procedure of matching the income with the expenses is also bookkeeping. In addition, the preparation of income and expense statement is one of the accounting cycles. It should have the lists of income earned followed by the deductions or lists of expenses. Moreover, the difference between the two is the net income if positive and the net loss if negative.

The net income or net loss is the equity of the employee unless the employee has a business. Thus, there’s a need for the whole accounting process. If the basis of computation is an individual, the bookkeeping is similar to accounting. There is no need to prepare all the financial statements and interpretations for other users for individual finances.

See more examples of income statements:

However, if the basis of computation is for business especially a corporation, the bookkeeping is not similar to accounting. It is not accounting as a whole because accounting is a three activity process. These are the bookkeeping process, the preparation of financial statements, and the interpretation or communication to end-users. The two remaining activities are more on following the accounting standards.

Accounting is a tool to measure financials. It explains the flow of your cash. Accounting determines whether you earned or lost something out of your effort or investment. It helps you decide for the future because by accounting you can make projections of your future income. You can also budget for your future expenses. In addition, you can weigh and measure every single thing in your business. For instance, the status of your business can be measured whether it is in the past present, or future. Moreover, you can even establish allowances in future events or circumstances that cannot be predicted with certainty. Accounting is a guide on how you will drive your business to get the desired business results.

Where Accounting Started

Accounting started when people start to trade what they have in exchange for other things. The most common work of people before was farming, fishing, and shepherding. Along with this, the way of trading is simple as one is to one. For example, trading crops in exchange for fish or farm animals. The trading before is regardless of value. Accounting as well is as simple as additions and subtractions of what you own or your assets.

Considering that the world changes oftentimes, simple trading needs enhancement. The trading improves and the exchange should be of equivalent values. With these, people used natural resources like gold silver, and bronze as the basis of measurement of exchange. This is because payment is portable and not consumable. The value of goods and services was based on demand and supply. Furthermore, in accounting the simple addition and deduction of assets (what you own) was enhanced as well. The basic standards were established or set to document the exchange.

Conclusion

In conclusion, as the world became civilized the natural resources as a means of payment were replaced by money. Money is legal tenders or banknotes. Despite civilization goods and services are still based on demand and supply. Nevertheless, the accounting standards should be congruent to the changes.

Every time there is a change, accounting standards will also change it might increase, decrease, or revised. For instance, the transition of natural resources like gold, silver, and bronze to paper bills should have proper accounting. It is because money is like a certificate of claims that corresponds to natural resources. Another example is the covid19 pandemic fortuitous events. People are turning more on to digital or online as a result of the pandemic. Moreover, accounting standards should update congruent to the digital world to provide accurate and reliable measurements of finances.

Related Blog: Bookkeeping Services

Need help with bookkeeping services? Contact us.

Pingback: How to Bookkeep: Banking Industry | Ronainph

Pingback: Debt Consolidation Calculator – Starts Countdown To Eliminate Debt – Site Title