This content aims to introduce you to change in accounting estimate. Several transactions are considered accounting estimate. Maybe you are wondering why it’s just an estimate. Moreover, maybe you have this question in your thoughts about how financial statements are reliable if some transactions are based on estimates. It is a good question to wonder. And in this content, I will enlighten you on how financial statements are still reliable considering some transactions are estimates. One example of accounting estimate is related to Property, plant, and equipment (PPE) which is depreciation. Depreciation is a way to allocate costs. An example of an asset account that depreciates is the property, plant, and equipment (PPE).

Most PPE has huge costs and is useful for more than one reporting period (1 year). It is illogical for the company to expense PPE outright because it performs for more than one reporting period. Moreover, PPE outright expense will result in a net loss for the company which violates the matching principle. The matching principle is an accounting standard that mandates matching expenses with its revenue. Since PPE is useful for several years means that its contribution to generates income is good for more than 1 year. In addition, the bureau of internal revenue (BIR) does not allow the recording of depreciable assets as an outright expense. Moreover, if the amount is material.

Depreciation change in accounting estimate

There is no accounting standard regarding the useful life of a PPE asset. The company decides what is the useful life of an asset. The company uses this asset for whatever purpose it may serve. Therefore, they are familiar with what useful life the specific PPE normally has. Companies normally make an assumption based on the historical life of specific PPE. The company also considers how often the PPE is used. Moreover, other related factors to arrive at what the estimated number will be. In addition, some instances and/or events will somehow result in wrong estimates. And to make reliable financial statements, the company decides to change the accounting estimates. A change in accounting estimates could be a change in useful life, residual value, or depreciation method.

The application of a change in the accounting estimate of depreciation is prospective. Prospective application means that the balances from the past will stay as-is. In addition, the change in accounting estimates applies to current and future transactions. The adjustment on the balances starts when there are changes in accounting estimates. No need to adjust previous balances.

Change in useful life

Some company changes the useful life of PPE when the company discovers that the asset will have a more or less useful life. Based on perspective application, any adjustments will be made in the current or future transactions (depreciation). When the company decides to add the useful life of a specific asset, the treatment is moving forward. The adjustment will be remaining balance over remaining useful life (new useful life minus years of depreciation equals the remaining useful life)

Illustration I:

CD company purchase a truck for P5,000,000 on August 18, 2021. The estimated useful life of the truck is 5 years, and the salvage value is P350,000. The company uses the straight-line method of depreciation.

In the third year, CD company encounters unexpected sales for two consecutive years. The truck was used more than its useful routine. CD company assess that the truck no longer has a useful life of 5 years but 4 years. The company decided to change the estimates from 5 years to 4 years on the third depreciation. The question is what will be the depreciation expense of the truck? Prepare a complete depreciation table.

Computation:

| Depreciation Expense | Carrying Amount | |

| Year 1 | P5,000,000-P350,000/5 = P930,000 | P5,000,000 – P930,000 = P4,070,000 |

| Year 2 | P930,000 | P4,070,000 – P930,000 = P3,140,000 |

| Year 3 | P3,140,000-350,000/2=P1,395,000 | P3,140,000 – P1,395,000 = P1,745,000 |

| Year 4 | P1,395,000 | P1,745,000 – P1,395,000 = P350,000 |

| Year 5 | No depreciation expense | P350,000 |

Note: In the first two years the depreciation is P930,000 using the straight-line depreciation method. Notice the change in accounting estimates. The remaining balance is allocated to the new remaining useful life. Remember that depreciation is a way to allocate the cost. Since there’s a change in estimates, there will also be a change in cost allocation on the agreed remaining useful life.

Change in depreciation method

In reality, most companies use the straight-line method of depreciation because it’s easy to compute. Some companies use the double declining method for the reason that as PPE depreciates, the output decreases. Moreover, the double-declining method of depreciation lowers taxes in earlier years. The double-declining method or acceleration method has higher depreciation in earlier years and lower in later years. It is allowed by the bureau of internal revenue (BIR) as long as the company can justify its method.

Nevertheless, there are factors that make the company change its method. For instance, if the company wants its financial statements to be realistic. The company will assess its PPE and use a method that is applicable to the performance of the PPE. If the depreciation method happens to be inappropriate, then the company will change the method. The changes will be accepted as long as the company can justify the change. There is no right or wrong in selecting the method of depreciation as long as it is justified.

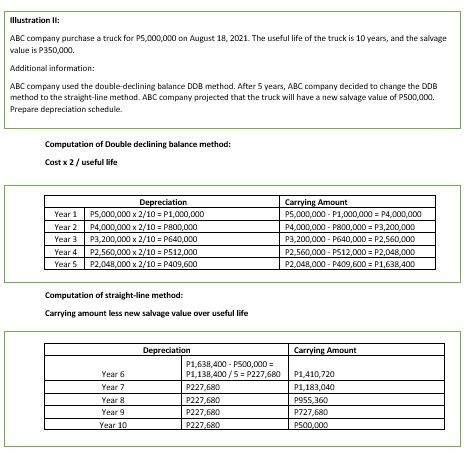

Illustration II:

ABC company purchase a truck for P5,000,000 on August 18, 2021. The useful life of the truck is 10 years, and the salvage value is P350,000.

Additional information:

ABC company used the double-declining balance DDB method. After 5 years, ABC company decided to change the DDB method to the straight-line method. ABC company projected that the truck will have a new salvage value of P500,000. Prepare depreciation schedule.

Computation of Double declining balance method:

Cost x 2 / useful life

| Depreciation Expense | Carrying Amount | |

| Year 1 | P5,000,000 x 2/10 = P1,000,000 | P5,000,000 – P1,000,000 = P4,000,000 |

| Year 2 | P4,000,000 x 2/10 = P800,000 | P4,000,000 – P800,000 = P3,200,000 |

| Year 3 | P3,200,000 x 2/10 = P640,000 | P3,200,000 – P640,000 = P2,560,000 |

| Year 4 | P2,560,000 x 2/10 = P512,000 | P2,560,000 – P512,000 = P2,048,000 |

| Year 5 | P2,048,000 x 2/10 = P409,600 | P2,048,000 – P409,600 = P1,638,400 |

Computation of straight-line method:

Carrying amount less new salvage value over the useful life

| Depreciation Expense | Carrying Amount | |

| Year 6 | P1,638,400 – P500,000 = P1,138,400 / 5 = P227,680 | P1,638,400 – P227,680 = P1,410,720 |

| Year 7 | P227,680 | P1,410,720 – P227,680 = P1,183,040 |

| Year 8 | P227,680 | P1,183,040 – P227,680 = P955,360 |

| Year 9 | P227,680 | P955,360 – P227,680 = P727,680 |

| Year 10 | P227,680 | P727,680 – P227,680 = P500,000 |

Change in accounting estimate of residual value

Change in residual value usually happens. It is because the economy changes from time to time. The estimates on the PPE acquisition are with the assumption of the present economy. Moreover, it considers the prediction of the economy in the future. The projections or assumptions could either be over or underestimates. As a result, the company adjusts based on economic status and what residual value of PPE will be realistic in succeeding years.

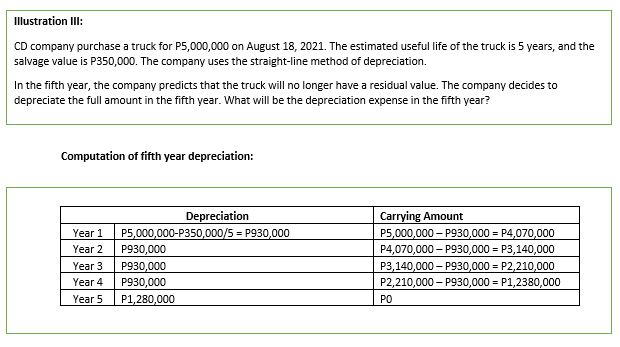

Illustration III:

CD company purchase a truck for P5,000,000 on August 18, 2021. The estimated useful life of the truck is 5 years, and the salvage value is P350,000. The company uses the straight-line method of depreciation.

In the fifth year, the company predicts that the truck will no longer have a residual value. The company decides to depreciate the full amount in the fifth year. What will be the depreciation expense in the fifth year?

| Depreciation Expense | Carrying Amount | |

| Year 1 | P5,000,000-P350,000/5 = P930,000 | P5,000,000 – P930,000 = P4,070,000 |

| Year 2 | P930,000 | P4,070,000 – P930,000 = P3,140,000 |

| Year 3 | P930,000 | P3,140,000 – P930,000 = P2,210,000 |

| Year 4 | P930,000 | P2,210,000 – P930,000 = P1,2380,000 |

| Year 5 | P1,280,000 | P0 |

Change in accounting estimate conclusion:

Accounting estimates are used in depreciating PPE with a useful life of more than 1 year and don’t have a fixed useful life. The goal of the estimates is to allocate the cost of PPE over its useful life congruent to its output. Although it’s just an estimate it doesn’t make the financial statements unreliable because the cost that is allocated is fixed. The only estimates are the method used, the residual value at the time of disposal, and useful life. These estimates don’t affect the PPE cost which is reliable in financial statements. Moreover, these estimates don’t violate accounting equations and accounting standards. Lastly, if the estimates are proven wrong in later years, the company can always amend or adjust its estimates to make them realistic.

Related Blog: Depreciation and Property Plant and Equipment

See more of change in accounting estimates examples