This content will teach you how bookkeepers/accountants record property, plant, and equipment transactions. The goal is to let you understand how the property, plant, and equipment presented in the financial statements turn out. This content provides illustrations of all the modes of acquisition. Especially the order of priority in determining the cost of PPE assets based on IAS or PAS. IAS stands for international accounting standards and PAS means Philippine accounting standards. IAS and PAS are almost the same, it only differs in terminologies used. Once you understand how the costing and valuation of each account are presented in financial statements, you can now do basic bookkeeping. You don’t have to read all the books in the accounting course. I’ll sort and filter it all for you. This website aims to teach the simplest and easiest way to anyone interested in bookkeeping/accounting.

IAS 16: Property Plant and Equipment

Property plant and equipment are tangible items that:

a.) are held for use in the production or supply of goods or services, for rental to others, or administrative purposes.

b.) are expected to be used during more than one period.

As stated in IAS 16. Tangible assets which mean it has physical existence or can be touch. Property, plant, and equipment are subject to depreciation. It is under long-term assets.

Note: IAS 16 does not apply to PPE classified as held for sale (IFRS 5), biological assets (except bearer plants, IAS 41), exploration and evaluation assets (IFRS 6), and mineral rights/reserves. IAS and IFRS are the same. The difference between them is IAS represents old accounting while IFRS represents new accounting. The reason we refer to IAS and IFRS is that these standards are adopted in the Philippines. Thus, PAS and PFRS function the same as IAS and IFRS. The difference between these standards are the terminologies used. Don’t be overwhelmed by the accounting standards mentioned in this blog. These are mentioned in special case transactions. But we will not go deep into special case transactions. We will only concentrate on the usual recording of property, plant and equipment cost, and valuations.

Examples of Property Plant and Equipment:

- Land

- Land Improvements

- Building

- Building Improvements

- Machinery

- Furniture and Fixtures

- Equipment

- Pattern, Molds, and Dies

- Tools

- Vehicles such as company motorcycles, cars, buses, airplanes, and ships

- Bearer plants

Measurement of Property Plant and Equipment

Initial measurement is the cost or purchase price, including directly attributable costs to bring the asset into use. Directly attributable cost like cost in bringing the asset to the location. Moreover, the initial cost of dismantling, removing, and restoration of the site (building), etcetera. Examples of directly attributable costs are delivery charges and installation costs.

Subsequent measurement – this is the measurement following the initial measurement. It is either a cost model or revaluation model. The cost model is computed as cost less accumulated depreciation and any accumulated impairment losses. The revaluation model is computed as a fair market value less any subsequent accumulated depreciation and impairment losses.

Modes of acquisition

1.) Cash basis Lump sum or basket purchase – bought property, plant, and equipment paid in cash. Lump-sum/basket purchase is the term used for buying a combination of two or more properties, plants, and equipment.

2.) On account subject to cash discount – accounts payable

3.) Installment – notes payable

4.) Issuance of share capital – equity instrument

5.) Issuance of bonds payable – a debt instrument

6.) Exchange – two firms exchange their property, plant, and equipment asset. Observing commercial substance in recording the cost of an asset. Commercial substance means different cash flows.

7.) Donation – shareholder or non-shareholder

8.) Government grant – given by the government

9.) Construction – applicable to building or machinery

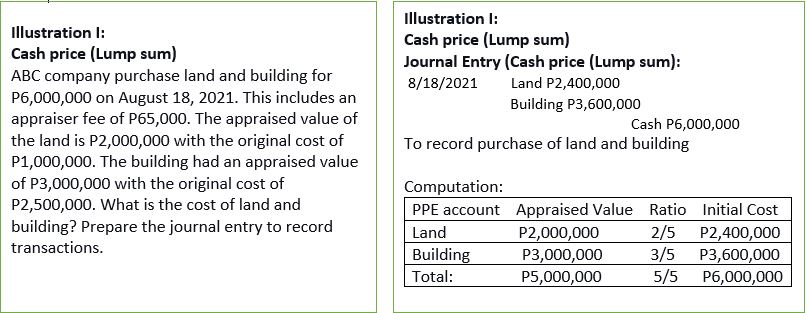

Illustration I:

Cash price (Lump sum)

ABC company purchase land and building for P6,000,000 on August 18, 2021. This includes an appraiser fee of P65,000. The appraised value of the land – P2,000,000 with the original cost of P1,000,000. The building had an appraised value of P3,000,000 with the original cost of P2,500,000. What is the cost of land and building? Moreover, prepare the journal entry to record transactions.

Insights:

In the accounting standard, the relative value is used in recording PPE. Relative value or relative fair market value – is not mentioned in the problem. The problem uses the appraised value. In this case, we will use the appraised value. The appraised value is the representation of relative value. The appraised value is the same as relative value, relative fair value, and fair market value. An example of directly attributable cost is the appraise fee. Directly attributable costs – are costs necessary to bring the asset to the location and condition necessary for an asset to be in use. Therefore, the appraiser fee is included in the cost of the PPE which is the land and building. Included because the appraisal is necessary for us to determine the value of the PPE.

Answer:

Get the ratio of land and building. We will use the appraised value as a basis. In this problem the ratio will be land (2/5) P2,400,000 and building 3/5) P3,600,000 computed as follows:

PPE account Appraised Value Ratio Initial Cost

Land P2,000,000 2/5 P2,400,000

Building P3,000,000 3/5 P3,600,000

Total: P5,000,000 5/5 P6,000,000

Journal Entry :

8/18/2021 Land P2,400,000

Building P3,600,000

Cash P6,000,000

To record purchase of land and building

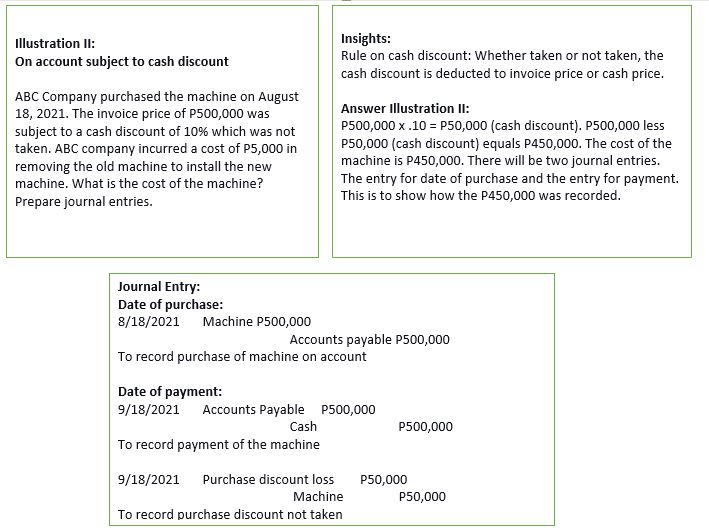

Illustration II:

On account subject to cash discount

ABC Company purchased the machine on August 18, 2021. The invoice price of P500,000 was subject to a cash discount of 10% which was not taken. ABC company incurred a cost of P5,000 in removing the old machine to install the new machine. What is the cost of the machine? Prepare journal entries.

Insights:

Rule on cash discount: The cash discount is deducted to invoice price or cash price, whether taken or not.

Answer:

P500,000 x .10 = P50,000 (cash discount). P500,000 less P50,000 (cash discount) equals P450,000. The cost of the machine is P450,000. There will be two journal entries. The entry for date of purchase and the payment entry. This is to show how the P450,000 was recorded.

Journal Entry:

Date of purchase:

8/18/2021 Machine P500,000

Accounts payable P500,000

To record purchase of machine on account

Date of payment:

9/18/2021 Accounts Payable P500,000

Cash P500,000

To record payment of machine dated August 18, 2021

9/18/2021 Purchase Discount Loss P50,000

Machine P50,000

To record purchase discount not taken

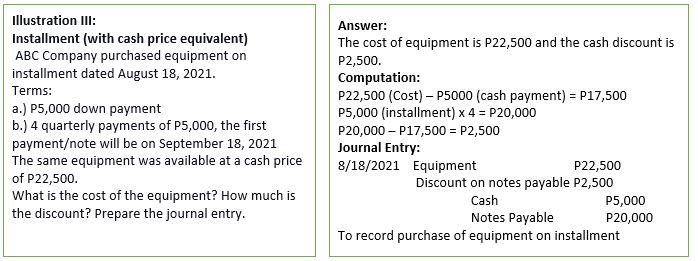

Illustration III:

Installment (with cash price equivalent)

ABC Company purchased equipment on installment dated August 18, 2021.

Terms:

a.) P5,000 down payment

b.) 4 quarterly payments of P5,000, the first payment/note will be on September 18, 2021

The same equipment was available at a cash price of P22,500.

What is the cost of the equipment? How much is the discount? Prepare the journal entry.

Insights:

On an installment mode of acquisition, when the cash price equivalent is available, the cash price equivalent will be the cost of PPE acquired.

Answer:

The cost of equipment is P22,500 and the cash discount is P2,500.

P22,500 (cost) – P5000 (cash payment) = P17,500

P5,000 (installment) x 4 = P20,000

P20,000 – P17,500 = P2,500 (cash discount)

Journal Entry:

8/18/2021 Equipment P22,500

Discount on notes payable P2,500

Cash P5,000

Notes Payable P20,000

To record purchase of equipment on installment

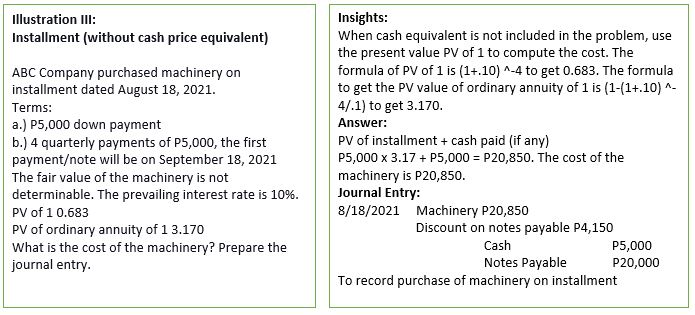

Installment (without cash price equivalent)

ABC Company purchased machinery on installment dated August 18, 2021.

Terms:

a.) P5,000 down payment

b.) 4 quarterly payments of P5,000, the first payment/note will be on September 18, 2021

The fair value of the machinery is not determinable. The prevailing interest rate is 10%.

PV of 1 0.683

PV of ordinary annuity of 1 3.170

What is the cost of the machinery? Moreover, prepare the journal entry.

Insights:

When cash equivalent is not included in the problem, use the present value PV of 1 to compute the cost. The formula of PV of 1 is (1+.10)^-4 to get 0.683. The formula to get the PV value of ordinary annuity of 1 is (1-(1+.10)^-4/.1) to get 3.170.

Answer:

PV of installment + cash paid (if any)

P5,000 x 3.17 + P5,000 = P20,850. The cost of the machinery is P20,850.

Journal Entry:

8/18/2021 Machinery P20,850

Discount on notes payable P4,150

Cash P5,000

Notes Payable P20,000

To record purchase of machinery on installment

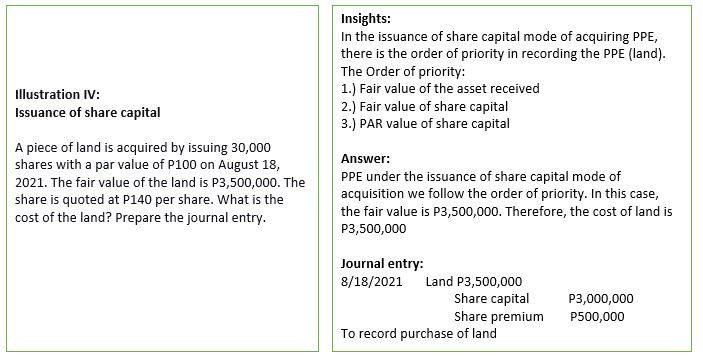

Illustration IV:

Issuance of share capital

A piece of land is acquired by issuing 30,000 shares with a par value of P100 on August 18, 2021. The fair value of the land is P3,500,000. The share is quoted at P140 per share. What is the cost of the land? Prepare the journal entry.

Insights:

In the issuance of share capital mode of acquiring PPE, there is the order of priority in recording the PPE (land).

The Order of priority:

1.) Fair value of the asset received

2.) Fair value of share capital

3.) PAR value of share capital

Answer:

PPE under the issuance of share capital mode of acquisition we follow the order of priority. In this case, the fair value is P3,500,000. Therefore, the cost of land is P3,500,000

Journal Entry:

Date of purchase:

8/18/2021 Land P3,500,000

Share Capital P3,000,000

Share Premium P500,000

To record purchase of land

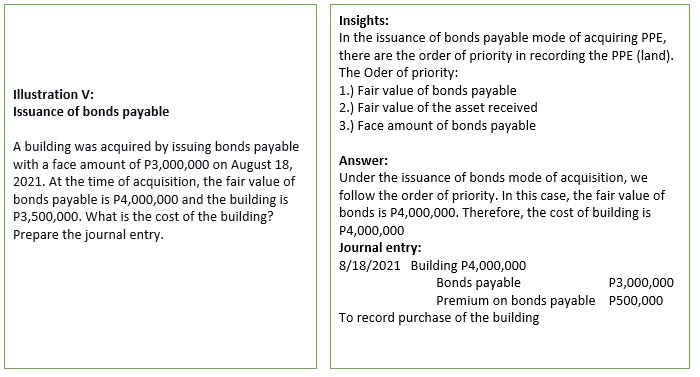

Illustration IV:

Issuance of bonds payable

A building was acquired by issuing bonds payable with a face amount of P3,000,000 on August 18, 2021. At the time of acquisition, the fair value of bonds payable is P4,000,000 and the building is P3,500,000. What is the cost of the building? Prepare the journal entry.

Insights:

In the issuance of bonds payable mode of acquiring PPE, there are the order of priority in recording the PPE (land).

The Oder of priority:

1.) Fair value of bonds payable

2.) Fair value of the asset received

3.) Face amount of bonds payable

Answer:

Under the issuance of bonds mode of acquisition, we follow the order of priority. In this case, the fair value of bonds is P4,000,000. Therefore, the cost of building is P4,000,000

Journal Entry:

8/18/2021 Building P4,000,000

Bonds Payable P3,000,000

Premium on Bonds Payable P500,000

To record purchase of the building

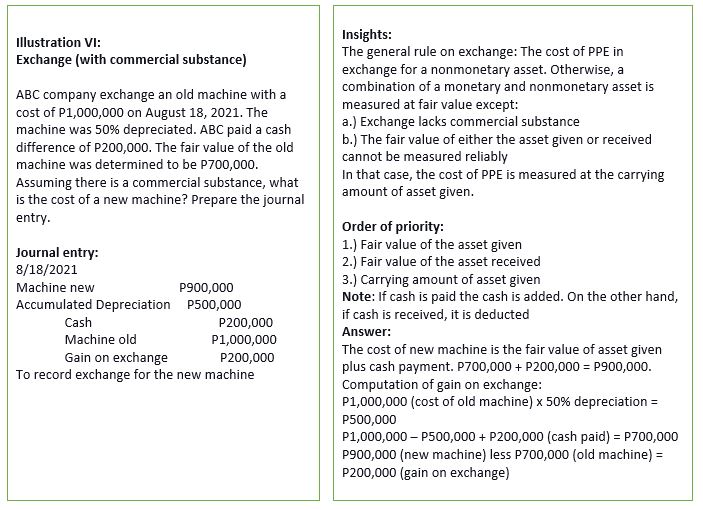

Illustration VI:

Exchange (with commercial substance)

ABC company exchange an old machine with a cost of P1,000,000 on August 18, 2021. The machine was 50% depreciated. ABC paid a cash difference of P200,000. The fair value of the old machine was determined to be P700,000. Assuming there is a commercial substance, what is the cost of a new machine? In addition, prepare the journal entry.

Insights:

The general rule on exchange: The cost of PPE in exchange for a nonmonetary asset. Otherwise, a combination of a monetary and nonmonetary asset is measured at fair value except:

a.) Exchange lacks commercial substance

b.) The fair value of either the asset given or received cannot be measured reliably

In that case, the cost of PPE is measured at the carrying amount of asset given.

Order of priority:

1.) Fair value of the asset given

2.) Fair value of the asset received

3.) Carrying amount of asset given

Note: If cash is paid the cash is added. On the other hand, if cash is received, it is deducted

Answer:

The cost of new machine is the fair value of asset given plus cash payment. P700,000 + P200,000 = P900,000.

Computation of gain on exchange:

P1,000,000 (cost of old machine) x 50% depreciation = P500,000

P1,000,000 – P500,000 + P200,000 (cash paid) = P700,000

P900,000 (new machine) less P700,000 (old machine) = P200,000 (gain on exchange)

Journal Entry:

8/18/2021 Machine (new) P900,000

Accumulated Depreciation P500,000

Machine (old) P1,000,000

Cash P200,000

Gain on exchange P200,000

To record exchange for the new machine

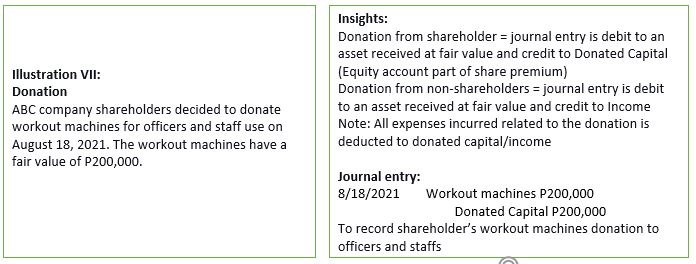

Illustration VII:

Donation

ABC company shareholders decided to donate workout machines for officers and staff use on August 18, 2021. The workout machines have a fair value of P200,000. What is the cost of the workout machine? In addition, prepare the journal entry.

Insights:

Donation from shareholder = journal entry is debit to an asset received at fair value and credit to Donated Capital (Equity account part of share premium)

Donation from non-shareholders = journal entry is debit to an asset received at fair value and credit to Income

Note: All expenses incurred related to the donation is deducted to donated capital/income

Journal Entry:

8/18/2021 Workout machines P200,000

Donated Capital P200,000

To record shareholder’s workout machines donation to officers and staff

Illustration VIII:

Government Grant

The government granted land to ABC charity for the construction of an additional school building for less fortunate children on August 18, 2021. The fair value of the land at the time of grant is P200,000.

Insights:

The same with a donation, the cost of PPE is measured at the fair value of the asset received plus directly attributable costs.

Journal entry:

8/18/2021 Land P200,000

Income P200,000

To record land government grant

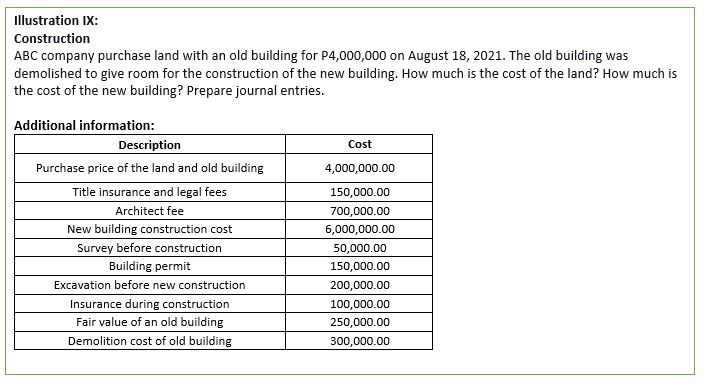

Illustration IX:

Construction

ABC company purchase land with an old building for P4,000,000 on August 18, 2021. The old building was demolished to give room for the construction of the new building. How much is the cost of the land? How much is the cost of the new building? Prepare journal entries.

Additional information:

| Description | Cost |

| Purchase price of the land and old building | 4,000,000.00 |

| Title insurance and legal fees | 150,000.00 |

| Architect fee | 700,000.00 |

| New building construction cost | 6,000,000.00 |

| Survey before construction | 50,000.00 |

| Building permit | 150,000.00 |

| Excavation before new construction | 200,000.00 |

| Insurance during construction | 100,000.00 |

| The fair value of an old building | 250,000.00 |

| Demolition cost of the old building | 300,000.00 |

Insights:

The cost of self-constructed PPE shall include:

1.) Direct cost of material (ex. Cement, steel, and hollow blocks)

2.) Direct cost of labor (construction workers)

3.) Indirect cost and incremental overhead (specifically identifiable and traceable to the construction) (ex. Foreman salary, utilities)

Examples of building construction costs:

- Raw material (cash discount taken or not is a deduction)

- Building permit

- Architect fee

- Superintendent fee

- Excavation cost

- Temporary building cost (shelter for construction workers and raw materials)

- Expenditures incurred during construction such as interest on construction loans and insurance

- Expenditures for equipment and fixtures made a permanent part of the structure

- Cost of temporary safety fence around the construction site and cost of subsequent removal thereof

- Safety inspection fee

Philippine Interpretation Committee (PIC) Interpretation on land and building

1.) Land and old building purchased at a single cost

a.) If the old building is usable, the single cost is allocated between the land and building based on relative fair value

b.) If the old building is unusable, the single cost is allocated to land only

2.) The old building is demolished to make room for the construction of the new building

a.) Any allocated carrying amount of the usable old building is recognized as a loss

b.) The demolition cost less salvage value is included as the cost of the new building

3.) The old building is demolished to prepare the land for the intended use but not to make room for the construction of the new building

a.) Any allocated carrying amount of the usable old building is recognized as a loss

b.) The demolition cost less salvage value is included as the cost of the land

Answer:

The cost of the land is P3,950,000 and the new building is P7,450,000.

Computed as follows:

Land (P4,000,000 less fair value of old building P250,0000) + P150,000 (title insurance) + P50,000 (survey before construction) = P3,950,000

New building P 6,000,000 + P700,000 (architect fee) + P150,000 (building permit) + P200,000 (excavation cost) + P100,000 (insurance) + P300,000 (demolition cost) = P7,450,000.

Journal entry:

8/18/2021 Land P3,950,000

Building P7,450,000

Cash P11,400,000

To record purchase of land and building a new building

Conclusion:

Recording of Property Plant and Equipment varies depending on the mode of acquisition. Moreover, it is all subject to accounting standards. This is just one account of the many accounts in the financial statements. Now if you understand the measurement of this account title then you can also do bookkeeping. Bookkeeping and accounting is a simple addition and subtraction. The standards and guideline is what makes it difficult. Because you have to know the standards and guidelines before coming up to what arithmetic operation to use. The illustrations somehow help you do so. The question is what’s next. You might want to check the related blog which is the depreciation expense.

Related Blog: Depreciation

Learn more about IAS / PAS 16

Do you have questions? Need help? Contact us

Pingback: Change in accounting estimate | Ronainph

Pingback: Depletion | Ronainph